Part 2 – Financial Planning with ASB, OD and Card Credit (Perancangan Kewangan dengan ASB, OD dan Kad Kredit)

<Get latest and more info about financial at www.bebas-hutang.com>

First I heard about Aziz CFP was from my friend, who actually heard from one of Aziz’s client. Because the story was not directly from the Aziz’s client, I didn’t get clearly how financial planning with Aziz will improve my financial status. Actually my friend who told me the story also couldn’t clearly understand what it is about.

What he told to me mostly like this. Apply OD (Overdraft), draw cash from Credit Card for your monthly expenses, then put all your salary into OD. The first thing that I was very concerned is about draw cash from Credit Card. By right we should avoid the CC.

Since my friend couldn’t explain much, plus he also didn’t really understand how it works, so I did research from internet. And I found one forum explaining more details. Let me summarize as below.

- Prepare some money in your ASB. Either from your saving or apply personal loan if you don’t have any saving.

- Convert ASB to Sijil, then apply OD with the Sijil.

- Once your OD approved, settle all your major loan.

- Bank in all of your income into OD account.

- Few days after that, withdraw 30~40% of your income’s amount from OD and put into your ASB account.

- Use Card Credit for your monthly expenses and must be within SD (Statement Date) and DD (Due Date).

- Pay amount used by CC on next month use OD.

- Duplicate from step 1 again every month.

Doesn’t make sense huh?…Actually they had explained more details, but I don’t want to share all the story here to avoid you guys get confuse and wrongly manage your financial. Financial planning is not something that you can try and error. Even 1 day will give you a different result.

So I tried to figure out how with my financial status. I did a simulation, via excel, via flowchart, but I still can’t figure out how this can improve my financial. And you have to apply all steps with specific amount and date…depends on your financial status. Finally I started to forget about it and keep all my research and simulation into one folder in my PC…to be continue…

read more at www.bebas-hutang.com

About CCRIS (Tentang CCRIS)

<Get latest and more info about financial at www.bebas-hutang.com>

CCRIS = Central Credit Reference Information System

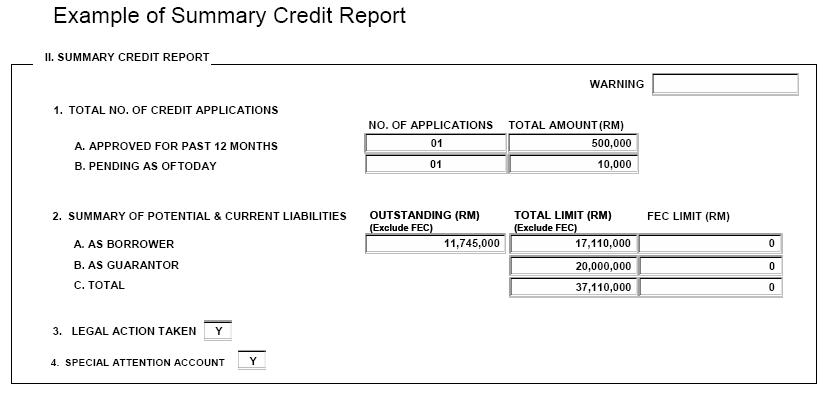

SUMMARY CREDIT REPORT

The Summary Credit Report displays summarised information relating to the

customer’s current and potential liabilities arising from credit facilities obtained

from the financial institutions in Malaysia. The liabilities include those where the

customer has obtained borrowings of its own, liabilities of joint-accounts, sole

proprietorships/partnerships/professional bodies in which the customer is an

Owner/Partner of the business. It also includes liabilities where the customer is a

guarantor for other borrowers.

How to check my CCRIS?

…read more at www.bebas-hutang.com

Part 1 – Experience with MLM

<Get latest and more info about financial at www.bebas-hutang.com>

In Malaysia, everybody knows what MLM is. It stands for Multi Level Marketing. How this business influences Malaysian people?…including me.

Since I first start working in 2003, until before I get married, my salary was just good enough for me. Even I can’t save much, but I still could make some saving. But it changed after I get married. My commitments were become different. There were a lot of things that we need when we are in a family. Then I realized that my current salary is not good enough for us to get better life. So what we did?

I started looking for side income. But I couldn’t do part time job at that time. I was an Engineer at one of Semiconductor Company in Kuala Langat. I always turn back late, even without OT…too bad huh!…but that was my first job…biasala, semangat lebih…haha.

So what we could do to get side income is by doing MLM. No need huge modal, with less than RM100, you can become a member. I joined few MLM…start from Elken, Amway, Network 21, and then Uptrend. The last one was JAI…most people said JAI is not MLM, but now the company’s account has been frozen by Bank Negara and charged illegal. I heard the company has been charged because they doing MLM business without a proper license. So now I considered JAI as MLM too.

What we get after few years with MLM? We lost our time, we lost few k especially with JAI, but we got a good lesson. In fact, none of my uplines in each MLM are really success with MLM after few years. Its not easy as what they keep said to me huh. Now I really 100% don’t believe with MLM or any other business that similar with it.

What I’m doing now? I’m doing financial planning, and hope can share with you guys how I clearing my debts. To be continue…

Apakah maksud Kaya

<Get latest and more info about financial at www.bebas-hutang.com>

Sebelum aku berjinak dengan perancang kewanganan, biasanya aku akan panggil orang yang pakai kerata besar, rumah besar itu orang kaya. Atau yang gaji 5 angka dan keatas. Tapi sekarang tidak lagi.

Tak kira berapa gaji seseorang itu, atau apa yang dia ada, samaada kereta besar, rumah besar, tapi kalau mereka juga mempunyai bebanan hutang seperti gadaian, pinjaman kereta atau kad kredit yang tak pernah langsai, mereka adalah sama sahaja seperti yang berpendapatan rendah.

Kekayaan adalah nilai bersih anda. Jika nilai keluar adalah sama atau melebihi nilai masuk, bagaimana anda dapat mengumpulkan kekayaan.

Mungkin anda akan berkata, “saya beli kereta BMW 3 series sebab saya mampu membelinya dengan gaji sekarang”…ok, fine..anda bergaji besar. Tapi anda tetap membayarnya setiap bulan bukan kan? Mungkin selama 7 hingga 9 tahun. Dan dengan pembelian BMW itu, peruntukan untuk simpanan sudah tiada…sama seperti masa anda bergaji kecil dan hanya memakai Proton Wira. Tanpa simpanan, bagaimana anda ingan mengumpulkan kekayaan?

Jadi ingat, kekayaan dinilai dari NILAI BERSIH, bukan pendapatan anda. Millionaire hanya akan dipanggil millionaire jika dia boleh mendatangani cek bernilai 1 million.

2 Jenis Hutang

<Get latest and more info about financial at www.bebas-hutang.com>

2 jenis hutang tu adalah Hutang Tertangung dan Hutang Lapuk.

Hutang Tertanggung:

Hutang yang diambil untuk membiayai aset yang bertambah nilainya, seperti harta tanah dan pendidikan.

Hutang Lapuk:

Hutang yang diambil untuk membeli barang yang tidak akan bertambah nilainya atau yang akan susut nilainya. Ini adalah benda-benda yang dibeli secara sewa beli seperti kereta, peralatan elektrik dan perabot.?

Jadi sekarang cuba imbas, hutang yang mana banyak bagi anda. Apa tunggu lagi…mari kita selesaikan semua Hutang Lapuk…tarak untung!!

Two Types of Debt

<Get latest and more info about financial at www.bebas-hutang.com>

Good Debt

Some of your debt might be considered as an investment. If the debt was incurred to purchase something that can be expected to go up in value and contribute to your overall financial health, then it’s very possible that such debt is good. A home purchase, for example, could very easily be considered as good debt. Since homes (generally) appreciate in value, the mortage loan that you incur to buy your house is actually an investment. Another example of good debt would be a student loan taken out to finance higher education. Obtaining a college degree usually means that you’ll make more money over the course of your lifetime.

Bad Debt

However, just as there is good debt, there are bad kinds of debt as well. When you use debt to finance things that can be consumed, you generally aren’t accumulating good debt. This is the type of debt that creates an unhealthy financial situation. Credit card debt is usually considered bad debt because of the nature of the items that credit cards are often used to purchase. It’s wise to avoid accumulating debt on everyday items such as clothes or food. If you use a credit card for these types of purchases, be sure to pay the card’s balance off in full each month (doing so will allow you to avoid costly interest charges).

When evaluating your debt and overall financial situation, it’s usually a good idea to focus on paying off your bad debts first. Since they provide no value, they’re more costly to carry than your good debts. Credit cards and auto loans (which generally have higher interest rates) should typically be paid off before tackling mortgages or student loans.

About Me